The landscape of retirement planning for government employees in India has undergone a massive shift with the introduction of a new framework that promises to settle the long-standing debate between market-linked returns and guaranteed security. For nearly two decades, the transition to the National Pension System (NPS) left many employees feeling vulnerable to the whims of the economy. The Unified Pension Scheme 2026 emerges as a definitive answer to these concerns, offering a hybrid model that ensures dignity and financial independence for those who have dedicated their lives to public service. By blending the contributory structure of modern finance with the solid guarantees of the past, the government has created a safety net that is both fiscally responsible and deeply empathetic to the needs of its workforce.

The Unified Pension Scheme 2026 is not just a policy update but a structural reimagining of how the state looks after its retirees. At its core, the scheme is designed to eliminate the uncertainty that came with purely market-dependent pensions. Under the Unified Pension Scheme 2026, employees are no longer left wondering what their monthly income will be once they hang up their boots. Instead, they are provided with a clear, predictable formula that guarantees 50% of their average basic pay as a pension, provided they meet the service milestones. This move has been widely seen as a “peace of mind” initiative, allowing central government employees to focus on their duties today, knowing that their tomorrow is anchored in a government-backed guarantee.

Unified Pension Scheme 2026

| Feature | Details |

| Scheme Name | Unified Pension Scheme (UPS) |

| Effective Date | April 1, 2025 (Primary Implementation Year 2026) |

| Primary Objective | To provide assured pension, family pension, and minimum pension |

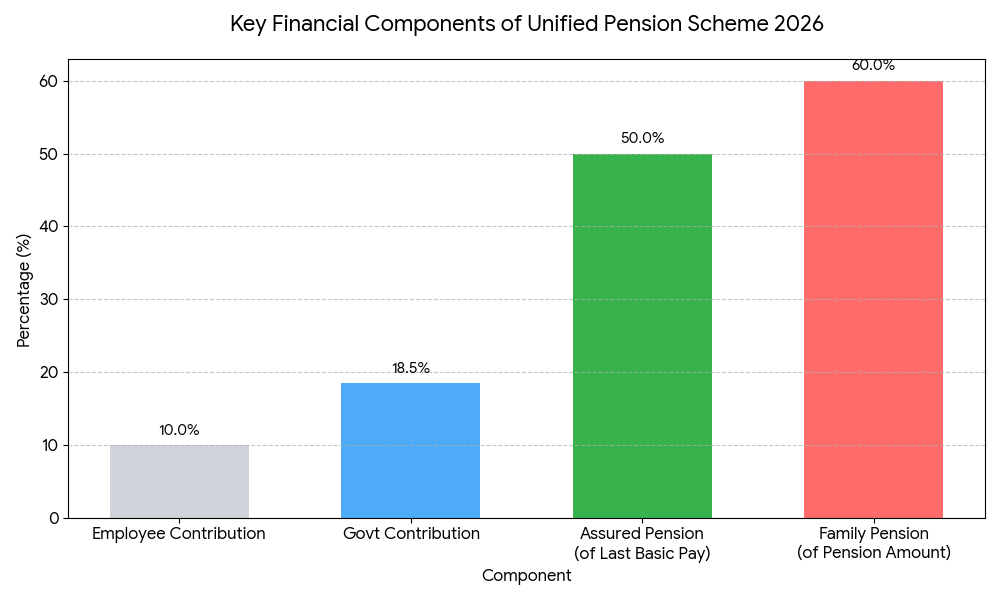

| Assured Pension | 50% of average basic pay of the last 12 months |

| Qualifying Service | Minimum 25 years for full pension, Pro-rata for 10-25 years |

| Assured Family Pension | 60% of the employee’s pension amount |

| Minimum Pension | 10,000 Per month after 10 years of service |

| Inflation Protection | Inflation indexation (Dearness Relief) applied |

| Government Contribution | Increased from 14% to 18.5% |

The Unified Pension Scheme 2026 is a landmark achievement in public policy. it successfully marries the need for fiscal discipline with the moral obligation to provide for those who serve the nation. It transforms retirement from a period of financial ambiguity into a period of earned rest and security. By guaranteeing a significant portion of the last-drawn salary and protecting it against the ravages of inflation, the government has created a gold standard for retirement benefits. As employees begin to navigate this new landscape, they can do so with the confidence that their financial future is no longer a gamble, but a promise kept by the state.

Key Pillars Of The Unified Pension Scheme

The architecture of the UPS is founded on five specific pillars that ensure an employee and their family are protected from the moment of retirement and beyond.

1. Assured Pension

The hallmark of this scheme is the 50% assurance. For any employee who has completed at least 25 years of qualifying service, the government guarantees a pension equal to half of the average basic pay drawn during the final year of their career. This provides a direct link between an employee’s career progression and their retirement lifestyle, ensuring that their standard of living does not drop abruptly.

2. Assured Family Pension

Social security is often measured by how it treats the most vulnerable members of a family. The UPS provides an Assured Family Pension, which grants 60% of the employee’s pension amount to the spouse or eligible dependents in the event of the pensioner’s death. This ensures that the household continues to have a steady stream of income even when the primary breadwinner is no longer there.

3. Assured Minimum Pension

Not every career spans three decades. Some individuals enter government service later in life or leave earlier due to personal reasons. To protect these individuals, the scheme guarantees a minimum pension of 10,000 per month for anyone who has served for at least 10 years. This acts as a poverty-prevention measure, ensuring that no former government servant is left without a basic subsistence income.

4. Inflation Indexation

Fixed pensions can be a trap in an inflationary economy. A sum that seems large today might barely buy groceries twenty years from now. The UPS solves this by applying “Dearness Relief” (DR) based on the All India Consumer Price Index for Industrial Workers (AICPI-IW). Just as active employees receive DA to offset inflation, pensioners will see their payouts increase as the cost of living rises.

5. Lump Sum Withdrawal At Retirement

Unlike previous systems where taking a lump sum might reduce your monthly pension, the UPS offers a separate payout. This is calculated as one-tenth of the monthly emoluments (pay plus DA) for every six months of service. This gives retirees a significant amount of capital to handle immediate post-retirement goals, like moving houses or settling debts, without touching their monthly guaranteed income.

Eligibility Criteria For UPS 2026

The government has made the eligibility for the UPS quite inclusive to ensure that as many people as possible can benefit from the transition:

- Central Government Employees: All current employees under the NPS have the option to switch to the UPS.

- New Joinees: Anyone entering service from April 1, 2025, onwards will have the choice between the market-linked NPS or the guaranteed UPS.

- Past Retirees: One of the most compassionate aspects of the scheme is that it extends to those who have already retired under the NPS since 2004. These retirees can opt into the UPS and may receive arrears for the difference in pension amounts.

- Voluntary Selection: The scheme is optional. Employees must actively choose to migrate to the UPS. If they prefer the potential high returns of the market-linked NPS, they are free to stay there.

How The UPS Differs From NPS And OPS

To understand why the UPS is a breakthrough, one must look at the historical context. The Old Pension Scheme (OPS) was a “defined benefit” plan where the government paid the entire pension without employee contributions. While great for workers, it was unsustainable for the national budget. The National Pension System (NPS) was a defined contribution plan, which was fiscally healthy but placed the risk of market crashes squarely on the employee’s shoulders. The Unified Pension Scheme 2026 is the bridge between these two worlds. It remains a contributory system employees still contribute 10% of their salary but the government has stepped up its commitment. By increasing the employer’s contribution to 18.5%, the government builds a larger fund that allows them to “guarantee” the 50% payout. Essentially, the government takes on the market risk so that the employee doesn’t have to.

Why The Unified Pension Scheme Is A Game Changer

The psychological impact of the UPS cannot be overstated. In an era where private-sector jobs are often volatile, government service has always been prized for its stability. However, the market-linked nature of the NPS had diluted that sense of security. The UPS restores the “social contract” between the state and its workers. Moreover, the UPS is a masterpiece of actuarial balance. By ensuring that pensions are indexed to inflation, the government is future-proofing the lives of millions. For the employee, it means their 50% pension stays meaningful throughout their old age. For the economy, it ensures that a large section of the elderly population remains consumer-capable, which is vital for long-term economic growth.

Transitioning To The New System: What Should Employees Do?

As we approach the full implementation in 2026, every eligible employee needs to make an informed decision. Here is a roadmap for that transition:

- Evaluate Your Service Length: If you have more than 25 years of service left, calculate your projected final basic pay. If the 50% guarantee gives you a figure you are comfortable with, the UPS is a safe harbor.

- Assess Your Risk Appetite: If you are comfortable with market fluctuations and believe the Indian equity markets will outperform the 50% guarantee significantly over the next few decades, the NPS might still be attractive.

- Review Family Needs: Consider the Family Pension aspect. The 60% guarantee for a spouse is often a deciding factor for those who are the sole earners in their family.

- Watch For Official Circulars: The transition will require paperwork, including specific forms to opt out of NPS and into UPS. Keep a close eye on your department’s administrative notifications to ensure you don’t miss the deadline.

Read More:-

PM Kisan 22nd Installment Date Is Out — Will You Receive ₹2,000 This Month? Full Details Inside!

FAQs on Unified Pension Scheme 2026

Is The UPS Better Than The NPS For Young Employees?

It depends on your perspective. The NPS offers the potential for a very large corpus if the markets perform well, which might lead to a higher pension.

What Happens If I Change Jobs From Government To Private Sector?

The UPS is specifically designed for government service. If you leave government service before the 10-year minimum mark, your pension eligibility under this specific scheme might be affected, though your contributions remain yours.

Can State Government Employees Join This Scheme?

The central government has designed this for its own employees, but they have invited state governments to adopt the same model.

How Is The 12-Month Average Calculated?

The Average Basic Pay is the mean of your basic salary over the last 12 months of your service. It does not include allowances, though the eventual pension will have Dearness Relief added to it.