When a child is born, parents instantly begin planning for years they cannot even see yet. Schooling, coaching classes, college admissions, professional degrees and sometimes even a wedding all of it arrives faster than expected. The problem most families discover late is not the planning itself, but the cost. Education expenses in India are rising every year, and what looks affordable today may feel overwhelming 15 years later. That is why structured financial tools like the SBI Child Plan 2026 are slowly becoming part of responsible parenting. The SBI Child Plan 2026 is designed to help parents convert small, manageable monthly savings into a dependable education fund. Many people still rely only on savings accounts, recurring deposits, or occasional investments. But those methods depend completely on continuous income. If income stops, savings stop too. A child future plan is built differently. It mixes insurance protection with disciplined long-term investment so the child’s future does not depend on the parent’s job stability or health. Instead of guessing how much money will be available later, families get a structured path.

The SBI Child Plan 2026 is a long-term child education and protection plan available through SBI’s insurance services. A parent pays regular premiums for a fixed number of years, and the policy builds a financial reserve for the child’s major milestones such as higher secondary education, graduation and early adulthood needs. The most important feature is the premium waiver benefit. If the parent passes away during the policy term, the insurer continues paying future premiums while the child still receives every benefit promised under the policy. Unlike a fixed deposit that gives one maturity amount, this plan distributes payouts at different life stages. That means the money comes when actually needed. Coaching fees at 16, college admission at 18 and career start support at 21 can all be covered in phases.

SBI Child Plan 2026

| Feature | Details |

|---|---|

| Type | Child insurance and savings plan |

| Investor | Parent or legal guardian |

| Child age eligibility | Birth to around 15 years |

| Premium payment | Monthly, quarterly or yearly |

| Policy duration | Approximately 10 to 25 years |

| Maturity benefit | Lump sum or milestone payouts |

| Protection | Life cover with premium waiver |

| Main objective | Education and future funding |

| Tax benefits | Available under current tax rules |

| Risk level | Low to moderate |

The SBI Child Plan 2026 is not designed to make parents wealthy. Its purpose is much more practical. It ensures that a child’s education continues without interruption even if life takes an unexpected turn. A small monthly contribution, maintained patiently over 15 to 20 years, can build a meaningful financial foundation. For many families, the real value is peace of mind. Parents cannot control inflation, job security or health, but they can control preparation. A structured child future fund replaces uncertainty with planning. The plan works best when started early and supported with additional investments. Ultimately, financial planning for children is not about chasing the highest return. It is about guaranteeing opportunity. When the time comes for college admission or career training, having funds ready can change a child’s confidence and choices. That is the real reason long term child plans continue to remain relevant.

Why Parents Consider Child Plans

- Education inflation in India is estimated close to 10 to 12 percent every year. A college course costing ₹10 lakh today may cross ₹25 lakh by the time a toddler becomes an adult. Because of this, parents no longer see child investment as optional.

- The SBI Child Plan 2026 attracts families mainly because it offers predictability. A bank deposit grows slowly and mutual funds fluctuate with markets. But a child plan focuses on goal based payouts. It is less about profit and more about certainty.

- The biggest relief for parents is protection. If the earning parent is no longer alive, the plan does not stop. The insurance company continues the premium payments and the child still receives all scheduled benefits. That removes the biggest financial risk a family faces.

How The Plan Actually Works

You decide three things first

- the child’s current age

- how long you want to invest

- how much premium you can comfortably pay

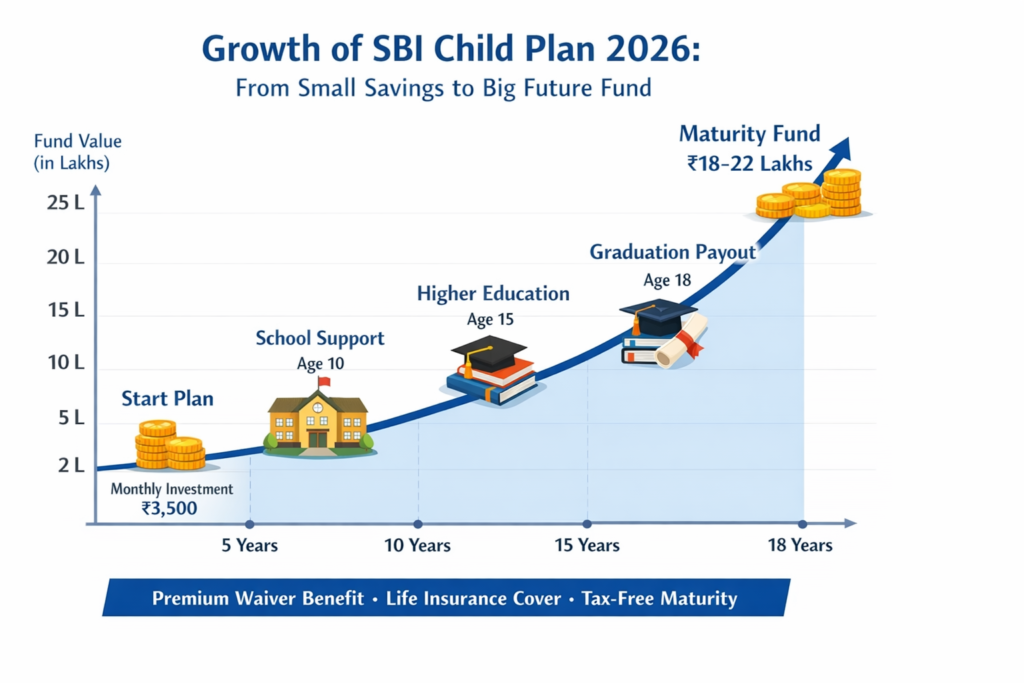

Then you start paying a fixed premium, even ₹2500 to ₹5000 per month works for many families. The SBI Child Plan 2026 gradually builds a corpus and releases money at pre decided stages. The payouts are structured around educational needs.

- Typical payout stages include

- secondary school support

- higher secondary education

- college admission

- final maturity fund

Because the money comes in phases, parents do not need to break other investments during important academic years.

Can A Small Monthly Investment Grow Big

Yes, and the reason is long term compounding.

Consider an example

- Monthly premium ₹3500

- Duration 18 years

- Total contribution roughly ₹7.5 lakh

Estimated maturity value can range between ₹15 lakh to ₹22 lakh depending on the policy type and bonuses. The SBI Child Plan 2026 grows through annual bonuses in traditional plans or market linked returns in certain variants. The earlier the policy begins, the stronger the effect of compounding. Starting when a child is 2 years old can create nearly double the corpus compared to starting at age 10.

Key Benefits

Premium Waiver Benefit

If the parent dies during the policy term, the insurer pays the remaining premiums. The child continues to receive all benefits without interruption. This feature alone differentiates the SBI child education plan from regular investments.

Life Insurance Protection

The family receives immediate financial support through a lump sum payout. It helps stabilize the household during a difficult time.

Milestone Based Payouts

Funds arrive exactly when education expenses arise, rather than at one distant maturity date.

Disciplined Savings Habit

Regular premium payments encourage long term consistency, something many families struggle to maintain independently.

Flexible Premium Options

Parents can pay monthly, quarterly or annually depending on income flow.

Tax Benefits

The SBI Child Plan 2026 also offers tax efficiency. Premium payments generally qualify for deductions under Section 80C within applicable limits. The maturity proceeds are typically tax free if policy conditions are met. This improves the real return compared to taxable fixed income investments.

Who Should Buy It

- This plan is most suitable for

- parents with children under 10 years

- single income households

- families wanting predictable education funding

- conservative investors who prefer security

It may not be ideal for people comfortable managing market investments or seeking aggressive growth through equity funds.

Risks And Limitations

Even a useful product has tradeoffs.

- Returns are usually lower than pure equity mutual funds.

- The policy requires long term commitment.

- Stopping early may reduce benefits.

Financial planners often recommend combining the SBI Child Plan 2026 with systematic investment plans in mutual funds. The plan provides safety while mutual funds provide growth.

How To Maximize Returns

- Start early before the child turns five.

- Choose a policy term extending until age 21.

- Avoid missing premiums.

- Add riders such as accidental cover.

- Increase premium as income grows.

Parents who follow a balanced strategy often use the SBI Child Plan 2026 as a guaranteed base and invest additional money into equity funds for higher potential returns.

Alternatives You Should Compare

Before purchasing, it is wise to compare with other long term options.

- Sukanya Samriddhi Yojana offers government backed savings for a girl child.

- Public Provident Fund provides stable long term returns.

- Mutual fund SIPs offer higher growth but no protection.

Child insurance plans sit between safety and growth, offering moderate returns along with life cover.

How To Apply

The process is straightforward.

- Choose a comfortable premium amount.

- Select policy duration based on child’s age.

- Complete KYC and documentation.

- Nominate the child as beneficiary.

- Begin premium payments.

The key rule is simple. Never select a premium that strains your monthly budget because consistency matters more than amount.

Read More:-

FAQs

Is SBI Child Plan 2026 Safe

Yes. It includes life insurance cover and structured payouts, making it safer than purely market dependent investments.

What Is the Minimum Premium

Premium usually starts around ₹2000 to ₹3000 monthly depending on duration and variant.

Can I Withdraw Money Early

Partial withdrawal may be allowed after a certain period, but it can reduce final maturity value.

Is The Maturity Amount Taxable

Generally, the maturity amount is tax free if policy conditions are satisfied under current tax rules.