The landscape of social welfare in the United Kingdom is about to undergo a massive transformation. For decades the Department for Work and Pensions has relied on a system of trust and individual reporting but that era is coming to a close. Government officials have confirmed that New DWP Bank Checks Announced: Millions of Claimants Could Be Affected by a fresh legislative push to modernize how benefit fraud is detected. This isn’t just a small policy update. It is a fundamental shift in the relationship between the state and the individual. The goal is to tackle the billions lost annually to error and fraud but the methods are sparking intense debate. For the average person claiming Universal Credit or Pension Credit this news can be unsettling. You might be wondering if your privacy is at risk or if a simple mistake could lead to your payments being frozen. The New DWP Bank Checks Announced: Millions of Claimants Could Be Affected headlines are flashing across news outlets because the scope of these powers is unprecedented.

We are moving from a system where the DWP needed suspicion to investigate a specific person to a system where banks will be asked to scan millions of accounts proactively. This article breaks down exactly what is happening and what it means for your wallet without the jargon. The government has been clear that the status quo is no longer sustainable. With fraud and error costing the taxpayer nearly ten billion pounds a year ministers have decided that stronger measures are required. This specific initiative is part of the Fraud Error and Debt Bill which gives the DWP new powers to compel banks to hand over data. The New DWP Bank Checks Announced: Millions of Claimants Could Be Affected initiative is designed to act as a safety net for the exchequer. It forces financial institutions to run monthly checks on their own customers who receive benefits. If a customer has savings that exceed the sixteen thousand pound threshold or if they show signs of undeclared income the bank must flag this to the DWP. It is a move from reactive investigation to proactive monitoring and it is set to change the rules of the game for millions of households across Britain.

New DWP Bank Checks

| Key Feature | Details |

| Legislation | Fraud Error and Debt Bill |

| Primary Target Benefits | Universal Credit and Pension Credit and ESA |

| Implementation | Phased rollout starting in 2026 |

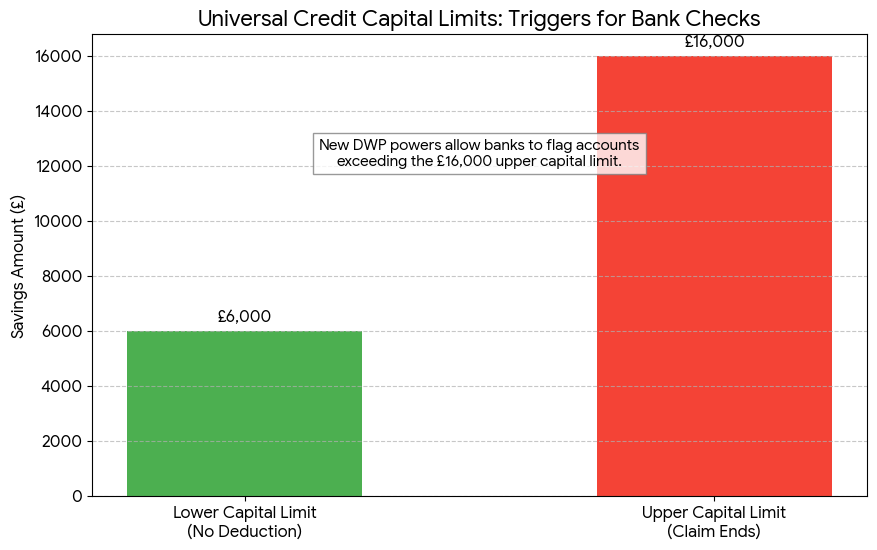

| Triggers | Savings over 16000 GBP and foreign transactions |

| Data Shared | Name and Date of Birth and Balance Flags |

| Oversight | Human review mandated before stopping pay |

Which Benefits Are Affected?

- The government is not rolling this out to every single person in the UK immediately. They are adopting a staged approach to ensure the technology works and to minimize disruption. The New DWP Bank Checks Announced Millions of Claimants Could Be Affected update highlights that means-tested benefits are the priority. These are the benefits where your financial situation directly dictates how much money you receive.

- Universal Credit is at the very top of the list. This benefit has the highest rate of overpayment due to the complexity of monthly reporting. Claimants are expected to report every change in income and savings but mistakes happen frequently. Under the new rules the DWP won’t have to wait for you to report a change. The bank will tell them if your savings dip into the danger zone.

- Pension Credit is another major area of focus. This benefit is a lifeline for the poorest pensioners but it also has strict capital limits. If a pensioner has savings over the limit they are not eligible. The DWP believes a significant amount of Pension Credit is paid out in error simply because savings are not declared. Employment and Support Allowance or ESA is also included in this first wave specifically the income-related portion.

- It is worth noting that the State Pension itself is currently excluded. The State Pension is based on your National Insurance record and not on how much money you have in the bank. Therefore scanning bank accounts for savings levels would be irrelevant for someone only receiving the State Pension. However disability benefits like PIP are also generally excluded for now as they are not means-tested either.

Can The DWP See My Bank Statements?

- This is the most common question and the source of the most anxiety. When people hear New DWP Bank Checks Announced Millions of Claimants Could Be Affected they often imagine a government worker sitting at a desk reading through their bank statement line by line. They worry about judgement on how they spend their money whether that is on cigarettes or alcohol or a subscription service.

- The reality is different and slightly more technical. The DWP will not have direct access to your bank account in real-time. They will not be able to see your transaction history or how you spend your money. Instead they are asking the banks to do the work. The DWP will provide a list of National Insurance numbers to the bank. The bank’s own computers will then scan the accounts associated with those numbers.

- The computer is looking for very specific “eligibility indicators.” These are simple yes or no questions. Does this account have more than sixteen thousand pounds in it? Has this account received money from abroad for more than four weeks? If the answer is no then the DWP hears nothing. If the answer is yes the bank sends a “flag” to the DWP. This flag contains your name and the fact that the limit was breached. It does not contain a list of your weekly groceries.

- This distinction is important because it protects a degree of privacy. The government is interested in whether you are eligible for the benefit and not in your lifestyle choices. However privacy campaigners argue that this is still a massive intrusion. They argue that scanning the accounts of innocent people to find the few who are breaking the rules treats every claimant like a suspect.

What Happens If The DWP Decides I Have Too Much Money In My Account?

- This refers to a scandal in Australia where automated systems wrongly accused thousands of people of owing money. The UK government has promised that this will not happen here. They have built safeguards into the New DWP Bank Checks Announced Millions of Claimants Could Be Affected legislation. If a bank sends a flag to the DWP your benefits are not stopped immediately. An automated system cannot take money away from you on its own. Instead the case is passed to a human case manager. This person will review the information and compare it with what you have declared.

- You will then be contacted. The DWP will write to you or call you to ask for an explanation. There are many valid reasons why a bank balance might look high for a short time. Perhaps you received a cost of living payment which is disregarded. Maybe you sold a house and are in the process of buying a new one which gives you a six-month grace period. You might have received a back payment of disability benefit which is also ignored for a year. You will have the chance to provide evidence. You can send in bank statements to prove that the money was a one-off payment or that it falls under a specific exemption. Only after a human being has looked at your evidence will a decision be made to stop your benefits or ask for money back. This human oversight is the main defense against computer errors destroying people’s finances.

When Will This Start?

Claimants do not need to panic right now. The New DWP Bank Checks Announced: Millions of Claimants Could Be Affected story is about legislation that is currently being passed. It is not yet live. The Bill needs to go through Parliament and become law which takes time. The DWP has outlined a phased timeline. They plan to start testing the system with a small number of banks in 2026. This initial phase is a pilot to see if the technology works and if the data is accurate. They want to avoid a situation where thousands of people are flagged incorrectly.

Full rollout to all major banks is expected to take several years. The top fifteen banks in the UK which handle ninety-seven percent of all benefit claimant accounts will be brought on board gradually. This means that for most people nothing will change in 2025. You should continue to report your income and savings as normal. However the delay does not mean you should ignore the rules. The DWP can already check bank accounts if they have a specific suspicion of fraud. The new powers simply allow them to do it on a massive scale without needing a specific reason first. The best preparation is to ensure your declarations are up to date today.

Why Is The Government Doing This?

- The driving force behind the New DWP Bank Checks Announced Millions of Claimants Could Be Affected plan is financial. The UK is facing a tight fiscal environment and every penny counts. The government argues that it is unfair for honest taxpayers to subsidize those who are breaking the rules.

- Fraud and error have risen sharply since the pandemic. During the Covid crisis checks were relaxed to get money to people quickly. Now the government is trying to claw that control back. They believe that technology offers a way to do this efficiently. By automating the checks they can save money on administrative staff and catch problems much earlier.

- Critics however argue that the focus is wrong. They say that a large portion of the “error” is due to the DWP’s own complex rules which are hard for claimants to understand. They argue that the government should focus on simplifying the system and providing better support rather than investing in surveillance technology.

- Despite the opposition the government seems determined to press ahead. They view the modernization of the DWP as essential. Just as HMRC receives data from employers to tax people correctly the DWP believes it should receive data from banks to pay benefits correctly.

Read More:-

New £200 Relief Payment Released — Here’s Who Gets It? Are You Eligible

FAQs on New DWP Bank Checks

1. Will the DWP check the accounts of my partner or spouse?

Yes they will if you have a joint claim. When you claim Universal Credit as a couple your joint capital is what matters.

2. What if I have savings in multiple different banks?

The new system is designed to catch exactly this scenario. The DWP knows that some people try to hide money by spreading it across different accounts.

3. Is there a minimum amount that triggers a check?

The banks are looking for capital limits. For Universal Credit the lower capital limit is six thousand pounds.

4. Can I refuse to let the bank share my data?

No you cannot. This is a statutory requirement. The legislation overrides standard data protection contracts between a bank and its customer for this specific purpose.