For years, retirement advice in the United States followed a predictable script: work steadily, retire in your late 60s, and then begin collecting benefits. But that story is changing quickly. The conversation around Social Security claiming ages has become one of the most important financial topics for people approaching retirement. Many workers are realizing that Social Security claiming ages can shape not only their monthly income but their entire long-term financial security. The reason is simple. Retirement today looks very different from what it did a generation ago. Higher housing costs, medical bills, inflation, and longer life spans are forcing Americans to rethink when to start benefits. Instead of automatically waiting for full retirement age, millions are making strategic choices. Some file earlier because they must, while others delay deliberately to lock in higher payments for life.

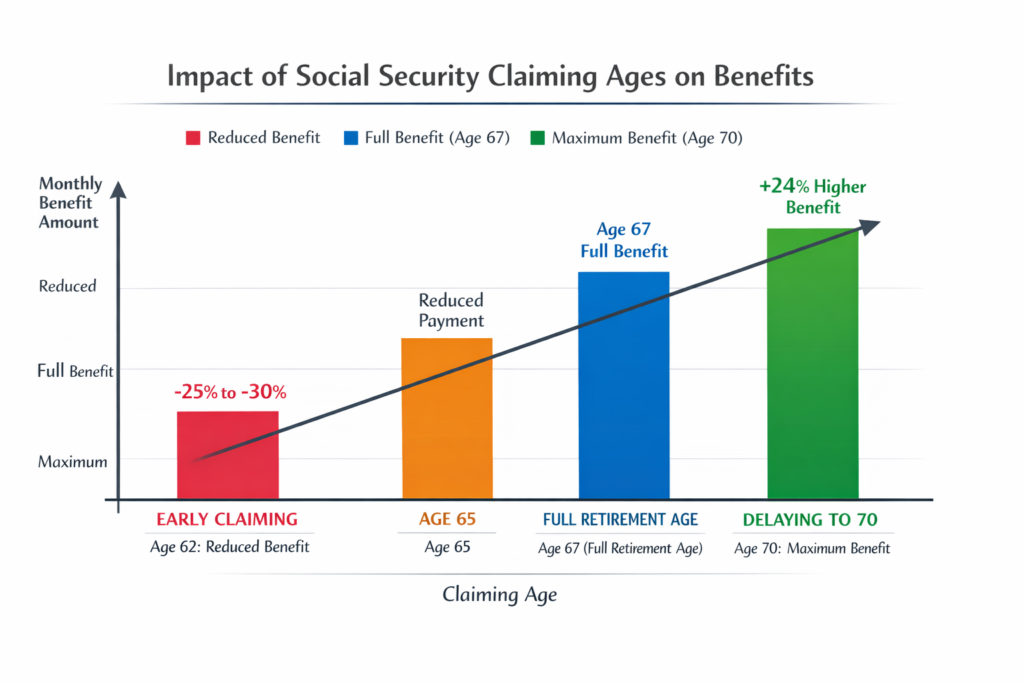

Understanding Social Security claiming ages has become essential before choosing a retirement plan. The earliest age to collect benefits is 62, but filing then permanently reduces your monthly payment. Full retirement age is now 67 for many workers born after 1960. Waiting beyond that increases payments every year until age 70. Retirement is no longer just about stopping work. It is a financial timing decision. Health, savings, employment stability, and family responsibilities all play a role in deciding the right filing age. Financial planners now consider this choice one of the most important financial decisions a person will ever make.

Goodbye To Retirement At 67

| Claiming Age | Benefit Adjustment | Monthly Payment Effect | Why People Choose It |

|---|---|---|---|

| 62 | 25–30% reduction | Smallest checks | Job loss, health concerns, immediate income |

| 65–66 | 6–13% reduction | Moderate payments | Transition into retirement |

| 67 | Full benefit | Standard payment | Financial stability |

| 68–69 | Increased benefit | Larger checks | Continued work |

| 70 | Up to 24% increase | Maximum lifetime income | Longevity planning |

Full Retirement Age Isn’t 65 Anymore

- One of the biggest surprises facing retirees is that 65 is no longer the age for full benefits. For workers born after 1960, full retirement age is 67. Many people still assume 65 is the target and end up filing early without realizing the long-term impact.

- Misunderstanding Social Security claiming ages can cost serious money. Filing even two years early can shrink benefits by more than ten percent. Over a retirement lasting 20 or 25 years, that difference can mean losing tens of thousands of dollars.

- The change happened gradually as Americans began living longer. The government needed benefits to last more years, so instead of cutting checks directly, it raised the full retirement age. The result is a system that rewards patience and planning more than ever before.

Why People Are Claiming Earlier

- Despite the reduction, many retirees still claim at 62. In most cases, this decision is driven by real-world circumstances rather than poor financial planning. The most common reason is employment. Older workers who lose jobs often struggle to find new ones. Once income stops and savings begin to fall, benefits become a necessity instead of a choice. Social Security claiming ages suddenly turn from a planning discussion into a survival decision.

- Health issues also play a major role. Someone dealing with chronic illness or physical limitations may prefer guaranteed payments now rather than larger payments later. For them, certainty matters more than maximizing lifetime totals. Family responsibilities are another major factor. Many older adults leave the workforce to care for aging parents, spouses, or even grandchildren. In those situations, Social Security becomes a replacement paycheck.

The Financial Trade Off

- The math behind Social Security claiming ages is simple but powerful. Claim early and you receive smaller payments for life. Wait longer and each monthly payment grows.

- For example, a worker eligible for $2,000 at full retirement age may receive roughly $1,400 at age 62. That difference continues every single month.

- However, delaying benefits after full retirement age increases payments by about eight percent annually until age 70. Waiting three extra years can raise payments by roughly one quarter. That increase is guaranteed and adjusted for inflation, which makes it extremely valuable in retirement planning.

- Many retirees underestimate how important stable income becomes later in life. Investment markets rise and fall, but Social Security continues every month.

The Growing Popularity of Delaying To 70

- A quiet shift is taking place. While early claims remain common, more financially prepared retirees are waiting longer. Understanding Social Security claiming ages allows them to treat benefits as long-term insurance rather than immediate income.

- This strategy works especially well for married couples. Often, the higher-earning spouse delays benefits so the surviving spouse will receive a larger payment later. Retirement today often lasts 25 to 30 years, and guaranteed income becomes more valuable as people age.

- Financial advisors increasingly recommend delaying when possible because the biggest retirement risk is not market losses. It is outliving savings.

Health And Longevity Are Driving Decisions

- The correct filing age often depends on expected lifespan. A person in poor health may benefit from filing earlier. Someone healthy with a long family life expectancy often benefits from waiting.

- Healthcare costs also affect Social Security claiming ages decisions. Some retirees need income immediately to cover insurance premiums and medications. Others can delay because they remain employed and insured.

- Retirement planning is no longer about reaching a certain birthday. It is about matching income timing with real life needs.

The Psychological Side of Retirement Timing

Money explains much of the decision, but emotions matter too.

- Some people claim early because they fear the system might change in the future. Others want to enjoy their retirement years while they are still active. After decades of working, waiting longer feels risky emotionally even if financially logical.

- On the other hand, many delay retirement because work provides purpose. A job offers routine, social interaction, and mental activity. Retirement timing often reflects lifestyle goals as much as financial strategy. Understanding Social Security claiming ages helps retirees balance financial security with quality of life.

What Advisors Are Telling Retirees

- Financial planners rarely recommend a single retirement age anymore. Instead, they encourage personalized strategies.

- Common advice includes using savings first when possible, coordinating spousal benefits, considering taxes and Medicare costs, and delaying benefits if long life expectancy is likely.

- The biggest mistake advisors see is automatically claiming at 62 without analysis. Yet they also emphasize that early filing can be the right choice when income is needed immediately.

The New Reality Of Retirement

The traditional retirement timeline is fading. Instead of a fixed age, retirement now happens in stages.

- Some retirees work part time while receiving benefits. Others delay Social Security claiming ages while living off savings. Many shift careers before filing.

- Workers today understand that the age they start benefits matters just as much as how much they saved. Retirement is no longer a single moment. It is a financial strategy built around timing, health, and personal goals.

- The major lesson is simple. Retirement at 67 is no longer the default. People are designing their own timeline based on their circumstances. And as awareness grows, the decision about when to claim benefits may become the most important retirement choice of all.

Read More:-

FAQs on Goodbye to Retirement At 67

1. What is the best age to claim Social Security?

There is no universal best age. If you need income right away or have health concerns, 62 may make sense.

2. Does claiming early permanently reduce benefits?

Yes. Filing before full retirement age permanently lowers monthly payments and the reduction continues for life.

3. Can I work while receiving Social Security?

Yes, but if you claim before full retirement age and earn above certain limits, part of the benefit may be temporarily withheld.

4. Why do some retirees delay until age 70?

Waiting significantly increases monthly payments and provides higher survivor benefits for a spouse later.