Buying your first home once followed a predictable journey. You worked, saved carefully each month, and eventually built a deposit. Today it feels far more complicated. House prices have risen steadily, rents absorb a large portion of income, and traditional savings accounts grow slowly. That is why first-time buyers rushing to ISAs has become a genuine shift in behaviour rather than a passing financial trend. Buyers have realised they do not have to fight the savings battle alone. A structured savings system now helps them. As a result, first-time buyers rushing to ISAs is transforming how young professionals prepare for homeownership. Speak to mortgage advisers and they often say the same thing. Most first-time buyers could manage monthly repayments, but they struggle to cross the upfront deposit barrier. In many areas, a starter property requires roughly £23,000 or more before lenders will approve a mortgage. For years, this figure prevented thousands of renters from moving forward. Recently, buyers discovered that the challenge becomes manageable if the right savings approach is started early.

Interest in government-backed savings accounts has grown quickly in recent years. Higher borrowing costs and stricter affordability checks mean lenders reward borrowers who bring larger deposits. Because of this, first-time buyers rushing to ISAs are treating these accounts as part of mortgage planning rather than optional saving. A Lifetime ISA offers tax-free growth, a government bonus, and clear progress toward a deposit goal. Many people open one years before viewing properties. The purpose is simple. Build a reliable deposit and improve mortgage approval chances. Instead of waiting and hoping, buyers now plan their purchase timeline.

First-Time Buyers Are Rushing to ISAs

| Feature | Lifetime ISA | Help to Buy ISA | Standard Savings Account |

|---|---|---|---|

| Government bonus | 25% yearly | 25% at purchase | None |

| Annual saving limit | £4,000 | Monthly capped | Unlimited |

| Tax on interest | No | No | Yes above allowance |

| Property value limit | £450,000 | Lower historic caps | No limit |

| Withdrawal restriction | Yes | Yes | No |

| Best purpose | First home deposit | Supplement savings | General saving |

The £23,000 Deposit Problem

- Understanding the trend requires understanding the numbers. A property priced around £230,000 usually needs a 10 percent deposit. That places buyers immediately near the £23,000 threshold. Saving that amount while paying rent, bills, and daily expenses is challenging.

- Someone saving £300 per month would need more than six years to reach the goal. During that time, property prices may rise again. Many buyers describe the experience as saving constantly while the target keeps moving further away.

- This explains the rise of first-time buyers rushing to ISAs. The government bonus changes the process. Savers no longer rely only on their own contributions. Extra funds are added automatically, helping them reach the deposit faster.

How The Lifetime ISA Actually Works

The Lifetime ISA is simple to understand.

- You can deposit up to £4,000 per year.

- The government adds 25 percent.

- The maximum bonus equals £1,000 annually.

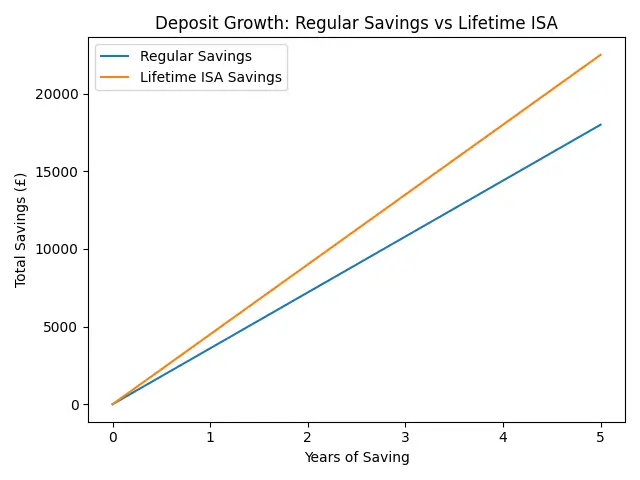

Saving £4,000 turns into £5,000. Repeating this over five years adds £5,000 in bonuses alone. This benefit is the main reason first-time buyers rushing to ISAs has increased. It effectively shortens the savings journey by years. Another advantage is tax protection. Interest earned is tax free, meaning all growth contributes directly to the deposit.

Cash Vs Stocks & Shares LISA

There are two main versions of the account and choosing the right one matters.

- Cash LISA

- Stable growth

- No market risk

- Suitable for buyers planning within five years

- Stocks and Shares LISA

- Invested in financial markets

- Higher growth potential

- Better for long-term saving

Most near-term buyers prefer the cash option. When the purchase date approaches, certainty becomes more important than potential investment returns. This cautious approach is typical among first-time buyers rushing to ISAs because protecting the deposit is essential.

What About The Help To Buy ISA

- Some people still hold Help to Buy ISAs. These accounts also provide a 25 percent bonus but operate differently.

- The bonus is paid at purchase completion. Monthly contributions were limited. You cannot combine the bonus with a Lifetime ISA.

- Because the newer account allows higher yearly contributions and clearer planning, buyers increasingly choose it. The continued growth of first-time buyers rushing to ISAs reflects this preference.

The Catch Withdrawal Penalties

- Before opening the account, one rule must be understood clearly.

- If you withdraw money for anything other than buying your first home or retirement after age sixty, a 25 percent charge applies.

- This removes the government bonus and part of the savings. The rule ensures the account is used for its intended purpose. Even so, it has not stopped first-time buyers rushing to ISAs because most savers open the account with a specific purchase goal.

Why Buyers Are Suddenly Rushing Into ISAs

Mortgage Rules Have Tightened

Lenders now place greater importance on deposit size. A larger upfront payment can significantly reduce monthly mortgage costs and improve approval chances.

Interest Rates Matter More

With borrowing costs higher than a few years ago, deposit size strongly affects repayments. Even a small increase in the deposit can noticeably reduce monthly payments.

Rent Is Blocking Savings

Rents have risen and leave little spare income. The government bonus acts like additional saving power. This financial pressure has encouraged first-time buyers rushing to ISAs.

How Buyers Are Maximising The Bonus

Successful savers follow consistent habits.

- They open the account early.

- They contribute regularly each month.

- They add extra funds before the April tax year deadline.

- They combine the ISA with another savings account for flexibility.

Consistency matters more than occasional large deposits. This steady strategy explains why first-time buyers rushing to ISAs continues to increase.

Common Mistakes To Avoid

- Opening the account too late: The account must be open for at least twelve months before a property purchase.

- Saving mainly outside the ISA: Keeping funds in standard accounts means missing bonus contributions.

- Ignoring the property price limit: The property must cost £450,000 or less to qualify.

Avoiding these mistakes helps buyers benefit fully from first-time buyers rushing to ISAs.

Is It Right For Every Buyer

- The Lifetime ISA suits buyers planning to purchase within a few years and under forty when opening. It works best for individuals with a clear property goal and stable income.

- It may not suit someone planning to move abroad, unsure of location, or buying immediately. Still, the increasing number of first-time buyers rushing to ISAs shows most people find it useful.

The Bigger Impact

- The rise in popularity reflects more than financial awareness. It represents a change in confidence. Homeownership once seemed distant for many renters. The deposit requirement created frustration and uncertainty.

- Now buyers have a structured path. Save regularly, receive bonuses, and track progress toward mortgage eligibility. The deposit challenge remains, but it feels achievable.

- Instead of wondering whether they will ever afford a home, buyers can calculate when. That is why the movement continues to grow. The £23,000 deposit barrier is no longer a permanent obstacle. With planning and the right tools, it becomes a realistic target within a few years.

Read More:-

First-Time Buyers Stunned by £4000 Stamp Duty Increase — The Hidden Cost No One Saw Coming

FAQs on First-Time Buyers Are Rushing to ISAs

Can I use it immediately to buy a property

No, the account must be open for at least twelve months before using it for a purchase.

Is it better than a regular savings account

For deposit saving, yes. The government bonus and tax-free interest provide stronger growth.

What happens if I withdraw early

A 25 percent charge applies unless the funds are used for a first home or retirement.

Can two buyers both open one

Yes. Each person can have their own account and combine bonuses to increase the deposit.