If you’re Earning Up To ₹20 Lakh In FY 2026-27, you’re standing at one of the most important financial crossroads of the year. The decision between the old tax regime and the new tax regime isn’t just about convenience anymore. It’s about real money. For salaried professionals Earning Up To ₹20 Lakh in FY 2026-27, even a small difference in deductions can change your final tax outgo by ₹40,000 to ₹60,000. Over the past few years, the government has made the new regime more attractive with simplified slab rates. But the old regime continues to reward disciplined investors and homeowners. So which one should you choose? The answer depends entirely on one factor how much deduction you can claim. Let’s break this down in a clear, practical way so you can make the smartest decision for FY 2026-27.

For individuals earning up to ₹20 lakh in FY 2026-27, the tax regime choice is not obvious. This income bracket sits exactly at the break-even zone where both regimes can work depending on deductions. The new regime offers lower slab rates but removes most exemptions. The old regime keeps benefits like Section 80C, 80D, HRA, and home loan interest intact. If your total deductions cross roughly ₹3.75 lakh to ₹4.25 lakh, the old regime usually becomes more tax-efficient. If your deductions are lower, the new regime may lead to reduced tax liability. Proper calculation is essential before deciding.

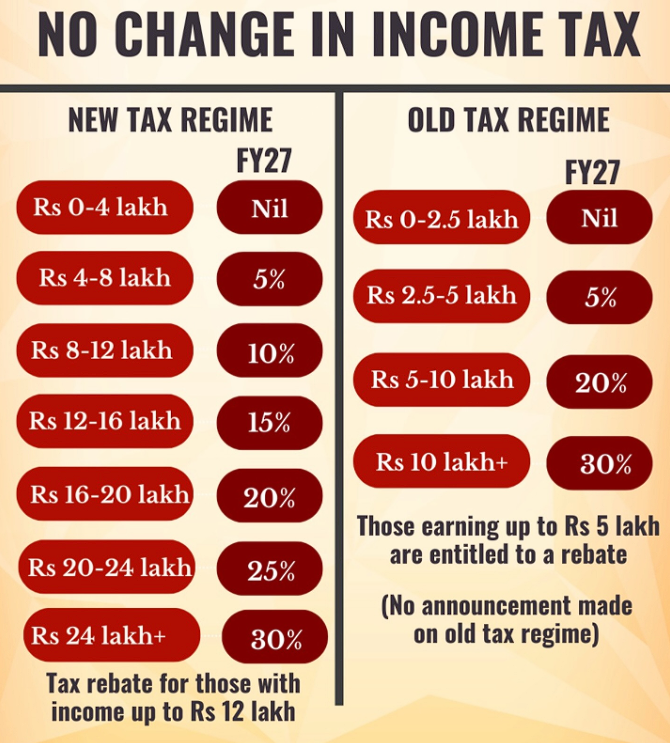

Earning Up To ₹20 Lakh In FY 2026-27

| Particulars | New Tax Regime FY 2026-27 | Old Tax Regime FY 2026-27 |

|---|---|---|

| Basic Exemption Limit | ₹3,00,000 | ₹2,50,000 |

| Standard Deduction | ₹50,000 | ₹50,000 |

| Section 80C Deduction | Not Available | Up To ₹1,50,000 |

| Section 80D Deduction | Not Available | ₹25,000 & ₹50,000 For Senior Citizens |

| Home Loan Interest | Not Allowed | Up To ₹2,00,000 |

| HRA Benefit | Not Allowed | Available |

| NPS 80CCD (1B) | Not Allowed | ₹50,000 Additional |

| Ideal For | Low Deductions & Simplicity | High Deductions & Structured Investments |

| Break Even Deduction | Not Applicable | Around ₹3.75 Lakh To ₹4.25 Lakh |

Old Tax Regime in FY 2026-27: When Does It Make Sense?

The old regime makes sense only if you actively use deductions. Without them, the higher slab rates under the old system will increase your tax burden.

- Let’s assume your gross annual income is ₹20 lakh.

- After the standard deduction of ₹50,000, your taxable income becomes ₹19.5 lakh in both regimes. The difference begins when you start applying deductions.

- If your total deductions are minimal, the new regime usually wins. But once your deductions move closer to ₹4 lakh, the old regime starts becoming financially smarter.

- This is why individuals earning up to ₹20 lakh in FY 2026-27 must calculate carefully instead of assuming the new regime is automatically better.

Tax Calculation At ₹20 Lakh Income

Let’s simplify the numbers for clarity.

Under The New Tax Regime

- Gross Income: ₹20,00,000

- Standard Deduction: ₹50,000

- Taxable Income: ₹19,50,000

With the revised slab structure, tax liability (before cess) generally falls between ₹2.1 lakh and ₹2.3 lakh.

There are no major deductions available beyond the standard deduction.

Under The Old Tax Regime

- Gross Income: ₹20,00,000

- Standard Deduction: ₹50,000

- Taxable Income: ₹19,50,000

Now assume the following deductions:

- Section 80C: ₹1,50,000

- Home Loan Interest: ₹2,00,000

- Section 80D: ₹25,000

- NPS 80CCD (1B): ₹50,000

- HRA Benefit: ₹75,000

- Total Deductions: ₹5,00,000

- Revised Taxable Income: ₹14,50,000

This reduction significantly lowers tax payable compared to the new regime. For someone earning up to ₹20 lakh in FY 2026-27, this difference can easily translate into savings of ₹40,000 to ₹70,000 depending on salary structure.

The Break Even Deduction Point

The key question is simple: how much deduction do you need?

Here’s the practical answer:

- If total deductions are below ₹3 lakh, the new regime is usually better.

- If deductions are between ₹3 lakh and ₹3.75 lakh, the comparison becomes close.

- If deductions exceed ₹4 lakh, the old regime typically becomes more beneficial.

For most taxpayers earning up to ₹20 lakh in FY 2026-27, the turning point lies around ₹3.75 lakh to ₹4.25 lakh in total deductions. Cross that mark, and the old regime generally starts delivering higher savings.

Key Deductions That Make The Difference

To make the old regime worth it, you must maximize eligible deductions strategically.

Section 80C

- Maximum limit: ₹1.5 lakh.

- This includes EPF contributions, PPF, ELSS mutual funds, life insurance premiums, and principal repayment of home loans.

- Most salaried individuals already contribute to EPF, which forms part of this limit.

Section 80D

Health insurance premiums qualify under this section.

- ₹25,000 for self and family.

- ₹50,000 additional for senior citizen parents.

This deduction improves both financial protection and tax efficiency.

Home Loan Interest Under Section 24

- Up to ₹2 lakh annually for self-occupied property.

- For many people earning up to ₹20 lakh in FY 2026-27, this single deduction pushes them into the old regime advantage zone.

National Pension System Under 80CCD (1B)

- Additional ₹50,000 beyond the 80C limit.

- This is often the final piece needed to cross the break-even threshold.

House Rent Allowance

If you live in a rented house and receive HRA, the exemption can significantly reduce taxable income, especially in metro cities.

When The New Regime Is Better

The new regime works better if:

- You do not have a home loan.

- Your total deductions remain below ₹3 lakh.

- You prefer higher take-home salary over locked-in investments.

- You want simplified tax filing without documentation hassle.

For younger professionals earning up to ₹20 lakh in FY 2026-27, especially those without housing loans or large investments, the new regime may provide better liquidity and lower immediate tax.

Practical Example Comparison

Let’s compare two scenarios.

Person A

- Total Deductions: ₹2.25 lakh

- Outcome: New regime results in lower tax by approximately ₹30,000.

Person B

- Total Deductions: ₹4.75 lakh

- Outcome: Old regime reduces tax by ₹50,000 or more.

This example highlights why the regime decision is purely numbers-driven.

Strategic Planning For FY 2026-27

If you are earning up to ₹20 lakh in FY 2026-27, tax planning should begin at the start of the financial year.

- Review your salary components carefully.

- Estimate annual deductions realistically.

- Avoid last-minute tax-saving investments made under pressure.

- Use updated tax calculators reflecting current slab rates.

Smart tax planning aligns tax savings with long-term financial goals instead of just reducing liability temporarily.

Should You Switch Every Year?

- Salaried individuals without business income can choose between regimes each financial year.

- This flexibility allows you to adapt. If your home loan ends or your investment pattern changes, your ideal regime may also change.

- That’s why taxpayers earning up to ₹20 lakh in FY 2026-27 should review the decision annually.

Read More:-

FAQs

1. How Much Deduction Is Required to Make the Old Tax Regime Better At ₹20 Lakh Income?

If you are earning up to ₹20 lakh in FY 2026-27, you generally need total deductions of around ₹3.75 lakh to ₹4.25 lakh to make the old tax regime more beneficial than the new regime.

2. Is The New Tax Regime Automatically Better for Salaries Up To ₹20 Lakh?

No, it is not automatic. The new regime works better if your deductions are low. However, if you claim benefits like Section 80C, 80D, home loan interest, HRA, and NPS contributions, the old regime may reduce your overall tax outgo.

3. Can I Switch Between the Old and New Tax Regime Every Year?

Yes. Salaried individuals without business income can choose between the old and new tax regimes each financial year.

4. Does A Home Loan Make a Big Difference in Choosing the Regime?

Yes, absolutely. The ₹2 lakh home loan interest deduction under the old regime is often the deciding factor. For many taxpayers earning up to ₹20 lakh, this deduction alone can push total savings beyond the break-even point.