Most people think building wealth requires a high income, a big business, or risky investments. In reality, financial security usually comes from something far simpler consistent saving. The Post Office Daily Saving Plan is based on this exact principle. You do not need lakhs of rupees to start. You only need discipline and patience. With the Post Office Daily Saving Plan, a small amount like ₹100 a day can gradually turn into a surprisingly large fund over the years. Look at your daily expenses honestly. A tea outside, a snack, an app subscription, or a quick food order easily costs ₹100 or more. We spend it without noticing. But if that same money is set aside daily and invested regularly, it quietly starts working for you. This is the reason post office schemes continue to attract millions of Indians even today. People trust security and stability more than flashy returns.

The Post Office Daily Saving Plan is not a separate official scheme with a daily counter at the post office. Instead, it is a smart saving method that uses existing post office investment accounts like Recurring Deposit and Public Provident Fund. You simply save ₹100 daily at home and deposit about ₹3,000 every month into a post office scheme. Over time, interest keeps adding and compounding multiplies your money. This method is ideal for beginners and conservative investors. You are not trying to predict stock markets or take financial risks. You are building wealth steadily. The biggest advantage is psychological. Small savings never feel stressful, so you stay consistent. And consistency is what actually creates the final large amount.

Post Office Daily Saving Plan

| Feature | Details |

|---|---|

| Daily Saving Amount | ₹100 |

| Monthly Deposit | ₹3,000 |

| Investment Options | Recurring Deposit or PPF |

| Average Interest | Around 6.7% to 7.5% |

| Suggested Tenure | 15 to 25 years |

| Estimated Maturity | Around ₹12 lakh |

| Risk Level | Very low, government backed |

| Tax Benefits | Available in PPF |

| Ideal For | Salaried employees, homemakers, beginners |

Financial success does not always come from earning more. Often it comes from managing what you already earn. A daily ₹100 saving seems insignificant today, but over the years it becomes a reliable financial support system. The Post Office Daily Saving Plan is powerful because it is simple. No complicated calculations, no market tracking, no constant monitoring. You just save regularly and allow time to grow your money. For retirement planning, children’s education, or emergency security, a steady method like this can be surprisingly effective. The real magic is not the interest rate. The real magic is consistency. If you start early and continue faithfully, the results will eventually surprise you.

What Is The Saving Concept Behind The Plan

The idea behind the Post Office Daily Saving Plan is simple but powerful. Instead of forcing yourself to invest a large amount, you break the process into tiny daily actions. Small daily savings are easy to maintain. Over one month, these small amounts become a proper investment installment.

Two financial forces make this plan work

- First is habit building. When saving becomes routine, you stop feeling the burden of investing.

- Second is compound interest. In compounding, you earn interest not only on your deposit but also on the interest earned earlier. Over long periods, this creates exponential growth.

In the beginning, progress looks slow. After several years, growth speeds up dramatically. Many investors are surprised that after 12 to 15 years, interest starts contributing more than their own deposits.

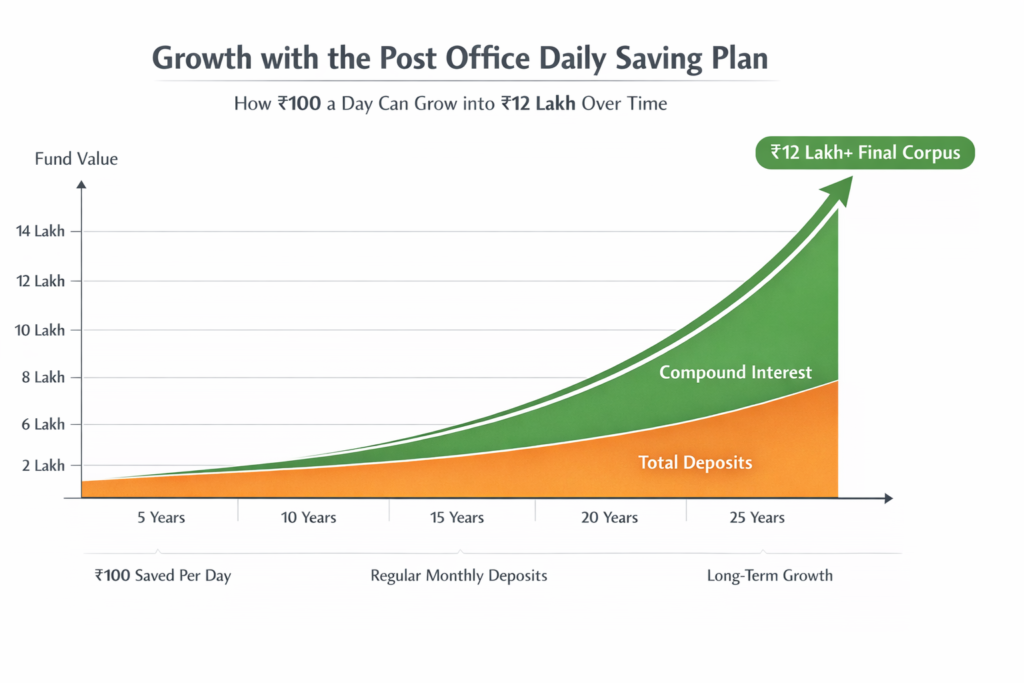

How ₹100 A Day Becomes A Big Fund

Let us understand this in a very practical way.

- Saving ₹100 daily equals ₹3,000 monthly.

- In one year, you invest ₹36,000.

Now imagine continuing this for many years in a compounding scheme like PPF.

- During the early years, your balance grows slowly. After about 8 to 10 years, you notice a difference. After 15 years, the growth becomes strong. The interest begins to generate large additions every year without increasing your contribution.

- Your total deposited money may be around five to seven lakh rupees depending on tenure. But the interest accumulated over time can push the maturity amount close to ₹12 lakh.

- The Post Office Daily Saving Plan proves that time is more important than amount. Starting early matters more than investing big.

Interest Rate and Tenure

Post office savings schemes are popular mainly because of predictable returns. Interest rates are declared by the government and revised periodically. Even with minor changes, they usually remain higher than a normal savings account.

Recurring Deposit

- A fixed amount is deposited every month.

- The maturity period is five years.

- You can extend it further.

- It suits medium term financial goals like buying appliances or building an emergency fund.

Public Provident Fund

- Lock in period is 15 years.

- Interest is compounded yearly.

- Maturity amount is tax free.

- Ideal for retirement planning and long term wealth.

For people following the Post Office Daily Saving Plan, PPF is often the stronger option because of tax free growth and long compounding period.

Who Should Consider This Plan

This plan is not only for investors. It is for ordinary people.

It suits

- Salaried employees who cannot save large amounts

- Homemakers who manage household expenses carefully

- Young earners starting their first job

- Small shop owners and self employed workers

- People who want safe investment options in India

Anyone who prefers security over risk will find this method comfortable. You do not need financial expertise to follow it.

How To Open The Account

Opening a post office account is simple and straightforward.

- Visit your nearest post office branch.

- Choose Recurring Deposit or PPF account.

- Fill the application form.

- Submit documents and initial deposit.

- Start monthly contributions.

Many people who follow the Post Office Daily Saving Plan keep a small box or envelope at home where they collect ₹100 daily and deposit monthly. This small trick helps maintain discipline.

Documents Required

You need basic identification documents:

- Aadhaar card

- PAN card

- Address proof

- Passport size photos

The process usually finishes the same day and your account becomes active quickly.

Advantages Of This Saving Method

Safety

Your money is backed by the Government of India. Market crashes do not affect your capital.

Low Entry Barrier

Anyone can begin with a tiny amount. No large starting investment required.

Stable Returns

You receive predictable growth without worrying about market fluctuations.

Tax Benefit

PPF investments qualify for tax deduction and tax free maturity.

Financial Discipline

The Post Office Daily Saving Plan develops a lifelong saving habit which is often more valuable than returns themselves.

Things To Remember

This is a long-term wealth plan, not a quick profit scheme.

- You should avoid stopping midway.

- Try not to miss monthly deposits.

- Be patient especially in early years.

Read More:-

Poultry Farm Loan 2026: Secure Fast Approval — Full Guide Inside!

FAQs on Post Office Daily Saving Plan

1. Is The Post Office Daily Saving Plan An Official Government Scheme

No. It is a saving strategy that uses post office investment accounts like RD and PPF by depositing monthly savings collected from daily money.

2. Can ₹100 Per Day Really Become ₹12 Lakh

Yes. Over long investment periods of 15 to 25 years, compound interest significantly increases the total value.

3. Which Account Is Better For This Plan

PPF is better for long-term tax-free wealth creation while RD is better for shorter savings goals.

4. Is My Money Safe

Yes. Post office investments are government backed and considered among the safest investment options in India.