If you rely on Social Security today, you already know one thing: inflation matters more than headlines. A few dollars at the grocery store or a small increase in electricity bills can quietly reshape a monthly budget. That is why the 2027 Social Security COLA forecast is getting so much attention. The 2027 Social Security COLA forecast points toward a noticeably smaller benefit increase than retirees have seen in recent years, and for many households, that difference could feel bigger than the percentage suggests. For retirees living on fixed income, Social Security is not extra spending money. It pays for groceries, medications, housing, and insurance. When benefit increases slow down while essential costs keep rising, people notice immediately. A modest annual adjustment can change how often someone fills a prescription, turns on the heat, or visits family. That is why this upcoming adjustment is more important than it first appears.

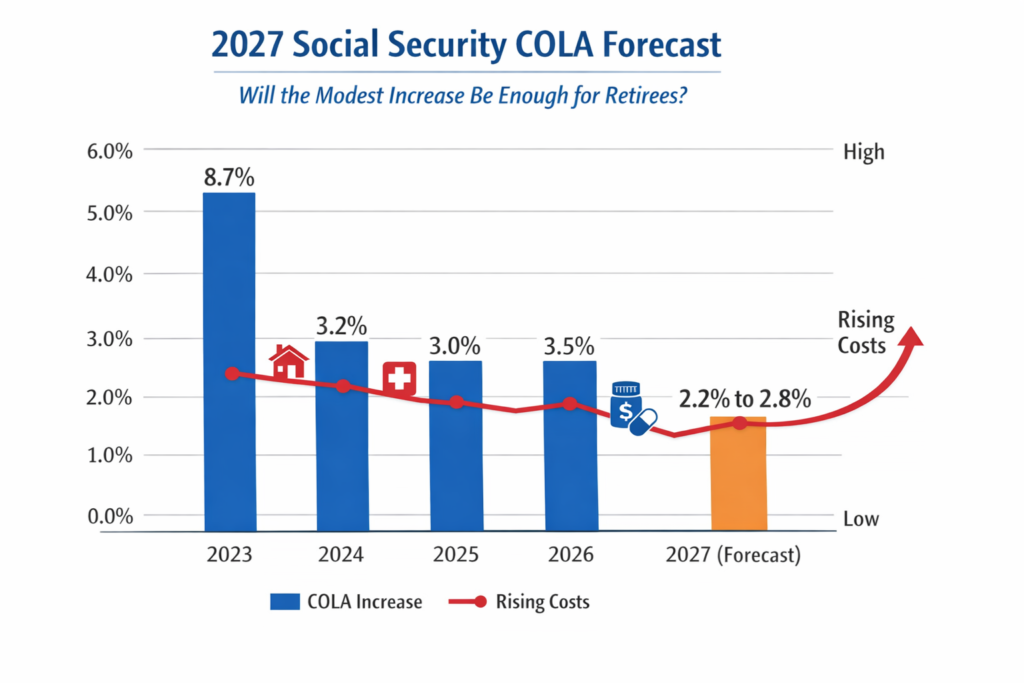

The 2027 Social Security COLA forecast currently suggests a cost-of-living adjustment of roughly 2.2 percent to 2.8 percent based on early inflation trends. The final number will depend on inflation data recorded between July and September of 2026, with the official announcement expected in October 2026 and new payments starting January 2027. While this range may seem normal historically, it comes after years of unusually high inflation adjustments earlier in the decade. Financial planners say the smaller increase does not necessarily mean lower expenses for retirees. Instead, it reflects broader economic cooling while real senior living costs, especially healthcare and housing, may continue to climb faster.

2027 Social Security COLA

| Key Factor | Current Early Estimate / Detail |

|---|---|

| Expected COLA Range | Around 2.2% – 2.8% |

| Inflation Index Used | CPI-W |

| Calculation Period | July–September 2026 |

| Official Announcement | October 2026 |

| Payment Change Begins | January 2027 |

| Reason for Lower Increase | Cooling inflation |

| Main Concern | Expenses rising faster than benefits |

Social Security remains one of the most reliable financial programs in the United States. Every year, benefits adjust automatically without requiring action from recipients. That stability is valuable. However, the upcoming adjustment offers a reminder. COLA is designed to maintain purchasing power, not improve lifestyle. Housing and healthcare costs often move independently of official inflation measurements. The 2027 Social Security COLA forecast does not predict a crisis. Instead, it underscores the importance of planning. Retirees who combine benefits with savings, budgeting, and healthcare planning will be better prepared for long term financial stability. The lesson is simple. Social Security is a foundation, not a complete retirement plan. A modest increase should encourage preparation, not panic.

How The COLA Is Actually Calculated

Many retirees believe the government simply chooses an annual increase. In reality, there is no negotiation or political vote involved.

- The Social Security Administration uses a fixed formula based on inflation. Officials compare inflation data from July, August, and September of one year to the same months from the previous year. If prices rise, benefits rise by the same percentage. If inflation is flat, benefits stay the same.

- The 2027 Social Security COLA forecast depends entirely on CPI-W, the Consumer Price Index for Urban Wage Earners and Clerical Workers. That detail matters. The index reflects working households, not retired households.

- Workers spend money on commuting, clothing, and payroll expenses. Retirees spend more on medical care and utilities. Because of that difference, a benefit adjustment that looks accurate on paper may not match real life expenses.

Why A Smaller Increase May Signal A Problem

- At first glance, lower inflation sounds positive. A smaller adjustment suggests prices are stabilizing. But for retirees, the situation is more complicated. Older adults typically spend a larger share of income on essential services. Medical costs alone can dominate a fixed budget. Prescription drugs, doctor visits, and insurance premiums do not always follow national inflation averages.

- Even if the 2027 Social Security COLA forecast lands near 2.5 percent, many retirees could still feel financially squeezed. If healthcare costs rise faster than the benefit increase, purchasing power effectively declines. This is the quiet challenge retirees face. The adjustment protects against general inflation, not personal inflation.

Inflation Has Cooled but Not for Everything

- The overall economy has seen inflation stabilize after earlier price spikes. Supply chains improved and energy markets became less volatile. However, several categories important to retirees remain expensive. Housing costs continue rising in many communities. Property taxes and rent rarely move in sync with national inflation averages. Home insurance premiums have increased sharply in several regions.

- Healthcare costs remain especially stubborn. Hospital services, medical testing, and prescription medications often increase faster than consumer goods. Because of this mismatch, the 2027 Social Security COLA forecast may look reasonable nationally while still feeling insufficient at home.

The Healthcare Factor

Healthcare may be the single biggest factor affecting how retirees experience a COLA increase. Medicare Part B premiums are typically deducted directly from Social Security benefits. When those premiums rise, the net increase shrinks.

- Imagine a retiree receiving $1,850 per month.

- A 2.5 percent COLA adds about $46 monthly.

- If Medicare premiums increase by $35 to $40, the real gain nearly disappears.

This is why retirees often say they received a raise but did not feel any difference in their bank account. When analysts discuss the 2027 Social Security COLA forecast, they always evaluate Medicare costs alongside it because the two are closely connected in real budgets.

Why Economists Are Paying Attention

Economists are not worried about the percentage itself. Historically, most COLA increases fall between 2 and 3 percent. From a macroeconomic perspective, the projected adjustment looks normal. What has changed is dependence on Social Security. Fewer retirees today have pensions compared to past generations. Personal savings rates vary widely, and people live longer. Many households now rely on Social Security for more than half their income. The 2027 Social Security COLA forecast matters more today than it would have decades ago because retirees have fewer backup income sources.

The Real Purchasing Power Issue

- Over time, retirees have gradually lost purchasing power even though COLA adjustments exist. The issue lies in how inflation is measured.

- The CPI-W index emphasizes goods like fuel and consumer products. Retirees spend more on services, especially healthcare. Services typically rise in price faster than goods.

- That means benefits technically keep pace with inflation statistics while still lagging behind real living costs.

- This underlying gap is why financial planners view the 2027 Social Security COLA forecast as a signal rather than just a number.

What Retirees Should Watch In 2026

The final adjustment will not be known until October 2026. However, several indicators will shape it.

- Monthly inflation reports provide early clues.

- Energy prices influence transportation and utilities.

- Housing costs affect overall inflation readings.

- Medical care inflation heavily impacts retirees.

If inflation rises suddenly, the final COLA could be higher. If stability continues, the 2027 Social Security COLA forecast will likely remain modest.

Planning Strategies For A Modest COLA

- A smaller benefit increase does not automatically create financial trouble. Preparation can make a major difference.

- Start by reviewing expenses once a year. Many retirees underestimate how much they spend on subscriptions, insurance, and maintenance.

- Maintain an emergency fund for medical or home repairs. Unexpected costs often cause more financial stress than inflation itself.

- Review Medicare plans annually. Coverage and premiums change every year, and switching plans can reduce costs.

- If possible, delaying Social Security claiming increases monthly benefits permanently. Even a small delay can significantly improve long term income.

- Supplementing income with savings withdrawals or part time work can also help offset slower benefit growth.

Is It Really A Warning Sign

The adjustment itself is not alarming. A 2 to 3 percent increase represents economic stability. The concern lies in how heavily retirees depend on one income source. For many Americans, Social Security covers essential expenses. When increases slow, financial flexibility disappears quickly. The 2027 Social Security COLA forecast highlights an important reality. Social Security protects against inflation in theory, but not always against the specific costs associated with aging.

Read More:-

Social Security Schedule Change Means Some Recipients Could Wait Months Between Checks

FAQs

When Will The 2027 Social Security COLA Be Announced

The official announcement is expected in October 2026 after the third quarter inflation data is finalized.

What Is the Estimated 2027 COLA Increase

Early projections suggest an increase between about 2.2 percent and 2.8 percent, depending on inflation trends in 2026.

Why Does the Increase Sometimes Feel Smaller Than Inflation

Because the calculation uses CPI-W, which tracks worker spending patterns rather than retiree expenses like healthcare.

Will Medicare Premiums Affect The Increase

Yes. Rising Medicare Part B premiums can reduce the net amount retirees actually receive after the adjustment.